How to save Tax for Income Tax Planning Guide Tax saving Tips eBook Download for AY 2021-22

How to Save Income Tax for FY 2022-2023 – Income Tax Planning Guide Tax saving Tips Download Tax Planning eBook for AY 2023-2024

# Updated Income Tax Software 2023 for AP &TS

# Income Tax Exemption Guide, Deduction Sections for 2023

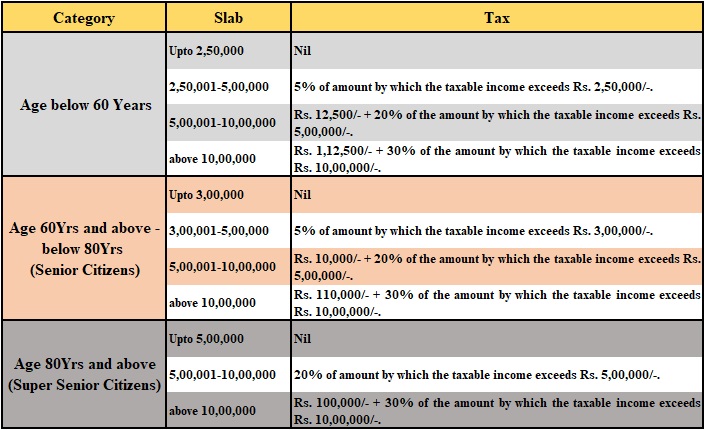

# Income Tax Slab Rates and Deductions for 2023

# Income Tax Planning Guide IT Software for AP/TS Teachers

Income Tax Rules 2022-2023

- Increased Tax Rebate u/s 87A: For individuals with net taxable income of Rs 5 lakh or less the tax rebate would be lesser of tax liability or Rs 12,500 whichever is lower

- Standard deduction for Salaried and Pensioners increased from Rs 40,000 to Rs 50,000

- Increased Tax for super-rich: Surcharge increased to 25% for income between 2 to 5 crore & to 37% for income beyond Rs 5 crores

- Additional Tax Deduction of Rs 1.5 lakhs u/s 80EEA on home loans on purchase of affordable home

- Additional Tax Deduction of Rs 1.5 lakhs u/s 80EEB on Auto loans on purchase of Electric vehicles

- No Tax on Notional Rental Income from Second House

- Capital gains exemption on reinvestment in two house properties: Tax payers can now buy two houses on sale of 1 house if the capital gains are less than Rs 2 crore. This benefit can be availed only once in lifetime

- TDS threshold increased from Rs 10,000 to Rs 40,000 on Bank Interest Income

You can download the tax planning eBook for FY 2019-20 by clicking the link below. As stated it covers all the income tax sections available for salaried and business tax payers:

Download Tax Planning eBook pdf

Tax saving Tips

Income Tax Software Programs for 2023

Click here to Download IT Suggestions in Telugu

IT Income Tax Approximate Tax details of Different Basic Pays for AP &TS Download

1. Section 80C/80CCC/80CCD

These 3 are the most popular sections for tax saving and have lot of options to save tax. The maximum exemption combining all the above sections is Rs 1.5 lakhs. 80CCC deals with the pension products while 80CCD includes Central Government Employee Pension Scheme.

You can choose from the following for tax saving investments:

- Employee/ Voluntary Provident Fund (EPF/VPF)

- PPF (Public Provident fund)

- Sukanya Samriddhi Account

- National Saving Certificate (NSC)

- Senior Citizen’s Saving Scheme (SCSS)

- 5 years Tax Saving Fixed Deposit in banks/post offices

- Life Insurance Premium

- Pension Plans from Life Insurance or Mutual Funds

- NPS

- Equity Linked Saving Scheme (ELSS – popularly known as Tax Saving Mutual Funds)

- Central Government Employee Pension Scheme

- Principal Payment on Home Loan

- Stamp Duty and registration of the House

- Tuition Fee for 2 children

- We have done a comprehensive analysis of all the above available options and you can choose which is the best for you.

2. Section 80CCD(1B) – Investment in NPS

Budget 2015 has allowed additional exemption of Rs 50,000 for investment in NPS. This is continued this year too. We have done a complete analysis which you can read by clicking the link below.

3. Payment of interest on Home Loan (Section 24/80EE)

The interest paid up to Rs 2 lakhs on home loan for self-occupied or rented home is exempted u/s 24. Earlier there was NO limit on interest deduction on rented property. Budget 2017 has changed this and now the tax exemption limit for interest paid on home loan is Rs 2 lakhs, irrespective of it being self-occupied or rented. However for rented homes any loss in excess of Rs 2 lakhs can be carried forward for up to 7 years.

Budget 2016 had provided additional exemption up to Rs 50,000 for payment of home loan interest for first time home buyers. To avail this benefit the value of home should not exceed Rs 50 lakhs and loan should not be more than Rs 35 lakhs.

4. Payment of Interest on Education Loan (Section 80E)

The entire interest paid (without any upper limit) on education loan in a financial year is eligible for deduction u/s 80E. However there is no deduction on principal paid for the Education Loan.

The loan should be for education of self, spouse or children only and should be taken for pursuing full time courses only. The loan has to be taken necessarily from approved charitable trust or a financial institution only.

The deduction is applicable for the year you start paying your interest and seven more years immediately after the initial year. So in all you can claim education loan deduction for maximum eight years.

5. Medical insurance for Self and Parents (Section 80D)

Premium paid for Mediclaim/ Health Insurance for Self, Spouse, Children and Parents qualify for deduction u/s 80D. You can claim maximum deduction of Rs 25,000 in case you are below 60 years of age and Rs 30,000 above 60 years of age.

An additional deduction of Rs 25,000 can be claimed for buying health insurance for your parents (Rs 30,000 in case of either parents being senior citizens). This deduction can be claimed irrespective of parents being dependent on you or not. However this benefit is not available for buying health insurance for in-laws.

HUFs can also claim this deduction for premium paid for insuring the health of any member of the HUF.

To avail deduction the premium should be paid in any mode other than cash. Budget 2013 had introduced deduction of Rs 5,000 (with in the Rs 25,000/30,000 limit) is also allowed for preventive health checkup for Self, Spouse, dependent Children and Parents. Its continued to this year too.

6. Treatment of Serious disease (Section 80DDB)

Cost incurred for treatment of certain disease for self and dependents gets deduction for Income tax. For very senior citizens (more than 80 years of age) the deduction amount is up to Rs 80,000; while for senior citizens (between 60 to 80 years of age) it Rs 60,000 and for all others its Rs 40,000. Dependent can be parents, spouse, children or siblings. They should be wholly dependent on you.

To claim the tax exemption you need a certificate from specialist from Government Hospital as proof for the ailment and the treatment. In case the expenses have been reimbursed by the insurance companies or your employer, this deduction cannot be claimed.In case of partial reimbursement, the balance amount can be claimed as deduction

Diseases Covered:

- Neurological Diseases

- Parkinson’s Disease

- Malignant Cancers

- AIDS

- Chronic Renal failure

- Hemophilia

- Thalassaemia

8. Physically Disabled Tax payer (Section 80U)

Tax Payer can claim deduction u/s 80U in case he suffers from certain disabilities or diseases. The deduction is Rs 75,000 in case of normal disability (40% or more disability) and Rs 1.25 Lakh for severe disability (80% or more disability)

A certificate from neurologist or Civil Surgeon or Chief Medical Officer of Government Hospital would be required as proof for the ailment.

- Disabilities Covered

- Blindness and Vision problems

- Leprosy-cured

- Hearing impairment

- Locomotor disability

- Mental retardation or illness

- Autism

- Cerebral Palsy

9. Physically Disabled Dependent (Section 80DD)

In case you have dependent who is differently abled, you can claim deduction for expenses on his maintenance and medical treatment up to Rs 75,000 or actual expenditure incurred, whichever is lesser. The limit is Rs 1.25 Lakh for severe disability conditions i.e. 80% or more of the disabilities. Dependent can be parents, spouse, children or siblings. Also the dependent should not have claimed any deduction for self disability u/s 80DDB.

To claim the tax benefit you would need disability certificate issued by state or central government medical board.

You can also claim tax exemption on premiums paid for life insurance policy (in tax payers’ name) where the disabled person is the beneficiary. In case the disabled dependent expires before the tax payer, the policy amount is returned back and treated as income for the year and is fully taxable.

40% or more of following Disability is considered for purpose of tax exemption

Blindness and Vision problems

Leprosy-cured

Hearing impairment

Locomotor disability

Mental retardation or illness

10. Donations to Charitable Institutions (Section 80G)

The government encourages us to donate to Charitable Organizations by providing tax deduction for the same u/s 80G. Some donations are exempted for 100% of the amount donated while for others its 50% of the donated amount. Also for most donations, the maximum exemption you can claim is limited to 10% of your gross annual income. Please note that only donations made in cash or cheque are eligible for deduction. Donations in kind like giving clothes, food, etc is not covered for tax exemption.

How to Claim Sec 80G Deduction?

A signed & stamped receipt issued by the Charitable Institution for your donation is must

The receipt should have the registration number issued by Income Tax Dept printed on it

Your name on the receipt should match with that on PAN Number

Also the amount donated should be mentioned both in number and words

11. Donations for Scientific Research (Section 80GGA)

- 100% tax deduction is allowed for donation to the following for scientific research u/s 80GGC

- To a scientific research association or University, college or other institution for undertaking of scientific research

- To a University, college or other institution to be used for research in social science or statistical research

- To an association or institution, undertaking of any programme of rural development

- To a public sector company or a local authority or to an association or institution approved by the National Committee, for carrying out any eligible project or scheme

- To the National Urban Poverty Eradication Fund set up

12. Donations to Political Parties (Section 80GGC)

100% tax deduction is allowed for donation to a political party registered under section 29A of the Representation of the People Act, 1951 u/s 80GGC. The maximum exemption you can claim is limited to 10% of your gross annual income

13. House Rent in case HRA is not part of Salary (Section 80GG)

In case, you do not receive HRA (House Rent Allowance) as a salary component, you can still claim house rent deduction u/s 80GG. Tax Payer may be either salaried/pensioner or self-employed.

To avail this you need to satisfy the following conditions:

The rent paid should be more than10% of the income

No one in the family including spouse, minor children or self should own a house in the city you are living. If you own a house in different city, you have to consider rental income on the same

The House Rent deduction is lower of the 3 numbers:

Rs. 5,000 per month [changed from Rs 2,000 to Rs 5,000 in Budget 2016]

25% of annual income

(Rent Paid – 10% of Annual Income)

You need to fill form no 10BA along with the tax return form

| S.NO. | INCOME TAX SOFTWARE | DOWNLOAD |

| 1 | IT Software 2019-20 for AP & Telangana for AY 2019-20 | Click Here |

| 2 | KSS Prasad Income Tax Software FY 2019-20 | Click Here |

| 3 | Putta Srinivas Reddy Income Tax Software FY 2019-20 | Click Here |

| 4 | Vijay Kumar Income Tax Software FY 2019-20 | Click Here |

| 5 | Zaheeruddin STO, Kakinada IT Software FY 2019-20 | Click Here |

| 6 | C.Ramanjaneyulu Income Tax Software FY 2019-20 | Click Here |

| 7 | B.Srinivasa Chary Income Tax Software FY 2019-20 | Click Here |

| 8 | Seshadri Income Tax Software FY 2019-20 | Click Here |

| 9 | Ramzan Ali Income Tax Software FY 2019-20 | Click Here |

| 10 | Mobile Version Income Tax Software FY 2019-20 | Click Here |

| 11 | Model School Teachers (APMS IT) Software FY 2019-20 | Click Here |

| 12 | DSC Wise Teachers IT Calculation Tables 2019-20 for AP, TS | Click Here |

| 13 | IT Softwares 2019-20 AP TS Teachers, Employees with PRC Arrears | Click Here |

| 14 | AP Employee Online Salary Details, Online Employee Pay Details | Click Here |

| 15 | TS Employees, Teachers Pay details, Month wise Salary Statement | Click Here |

| 16 | Telangana Employees Salary certificate | Click Here |

| 17 | How to Download SBI Home Loan Statement Interest and Principal | Click Here |

| 18 | How to Get LIC Premium Statements for Income Tax Purpose | Click Here |

| 19 | How to Pay PLI ( Postal Life Insurance ) Premium Online | Click Here |

| 20 | Tax Rebate u/s 87A Income Tax Exemption Guide | Click Here |

| 21 | Income Tax Slab Rates and Deductions Analysis for FY 2019-20 | Click Here |

| 22 | How to do Income Tax E-Filing Online Step by Step Process | Click Here |

| 23 | Income Tax e-Filing Processed (Confirmed) OR Not? Check Here | Click Here |

NEW in INCOME TAX 2020-21 (AY 2021-22)

- Section 87A: ప్రకారం పన్ను చెల్లించాల్సిన ఆదాయము 5లక్షల లోపు ఉన్న వారికి చెల్లించాల్సిన టాక్స్ లో రూ.12,500 లకు రిబేట్ సదుపాయాన్ని పెంచారు. ఈ సెక్షన్ ఉపయోగించుకుని 5లక్షల లోపు ఆదాయం కలిగిన వారు పూర్తి టాక్స్ మినహాయింపు పొందుతారు.

- Section 16 గత ఆర్థిక సంవత్సరం 2018-19కు నూతనంగా జీతం ద్వారా వచ్చిన ఆదాయంలో నుండి గరిష్టంగా Standard Deduction గా రూ.40,000 వరకు సెక్షన్ 16(ia) ద్వారా మినహాయింపునిచ్చారు దీనిని ఈ ఆర్థిక సంవత్సరం 2019-20కు 50,000 లకు పెంచారు.

ఆదాయముగా పరిగనించబడే జీతబత్యములు:

Pay, DA, HRA, IR, CCA, అలవెన్సులు, మెడికల్ అలవెన్సులు, అదనపు ఇంక్రిమెంట్ అలవెన్స్, సరెండర్ లీవు జీతం, పి.అర్.సి బకాయిలు, స్టెప్ అప్ ఎరియర్స్, సెలవు కాలపు జీతం, మొ. నవి ఆదాయంగా పరిగనించబడును.

ఆదాయముగా పరిగనించబడని అంశములు:

పదవి విరమణ తరువాత పొందే GPF/GIS/AP(TS)GLI లనుండి పొందే సొమ్ము మరియు నగదుగా మార్చుకున్న సంపాదిత సెలవులు, అర్దజీతపు సెలవుల పై వచ్చిన సొమ్ము, LTC పై పొందిన ప్రయాణ భత్యం, మెడికల్ రియంబర్స్మేంట్

మరియు GPF, AP(TS)GLI లలో అప్పుగా పొందిన సొమ్ము ఆదాయంగా పరిగణించరాదు.

మినహాయింపులు :

HRA మినహాయింపు : Under Section 10(13A) ప్రకారం క్రింది మూడు అంశంలలో ఏది తక్కువయితే ఆ మొత్తము ఆదాయం నుండి మినహాయింపు పొందవచ్చును.

1. పొందిన ఇంటి అద్దె బత్యం మొత్తం

2. ఇంటి అద్దెగా చెల్లించిన మొత్తం – 10% మూలవేతనం + డి.ఎ

3. 40% వేతనం

ఇంటి అద్దె అలవెన్స్ (HRA) నెలకు 3,000/- (సంవత్సరానికి సరాసరి 36,000/-) కన్నఎక్కువ పొందుతున్నవారు మొత్తం HRA మినహాయింపు పొందాలంటే రశీదు DDO కు సమర్పించాలి. చెల్లిస్తున్నఇంటి అద్దె 1లక్ష దాటిన పక్షంలో ఇంటి యజమాని PAN నంబర్ ఇవ్వాల్సి ఉంటుంది. స్వంత ఇంట్లో నివాసం ఉంటున్న వారికి HRA మినహాయింపు వర్తించదు.

Section 80GG: ఎలాంటి ఇంటి అద్దె భత్యం పొందని ఆదాయపు పన్ను చెల్లింపుదారులు తన పేరిట కాని, తన స్పౌజ్ పెరిట కాని, తన మైనర్ పిల్లల పేరిట కాని ఎక్కడ కూడా ఇల్లు లేని, అద్దె ఇంట్లో ఉంటున్న వారికి ఈ సెక్షన్ వర్తిస్తుంది

Section 16: ఈ ఆర్థిక సంవత్సరం 2019-20కు నూతనంగా జీతం ద్వారా వచ్చిన ఆదాయంలో నుండి గరిష్టంగా రూ.40,000 వరకు సెక్షన్ 16(ia) ద్వారా మినహాయింపునిచ్చారు.

ఇంటి ఋణం పై వడ్డి (Section24): ఇంటి ఋణం తో నిర్మించి స్వంతం గా ఉంటున్న వారికి ఋణం పై చెల్లిస్తున్న వడ్డి పై 2లక్షల వరకు మినహాయింపు కలదు. ఒక వేళ ఇల్లు బార్య మరియు భర్త ఇద్దరు జాయింటుగా ఋణం పొంది ఉంటె ఇద్దరికీ సమానం గా విభజించి ఒక్కొక్కరు గరిష్టంగా 2లక్షల మినహాయింపు పొందవచ్చు. ఇంటి ఋణం తీసుకున్న ఇంట్లో స్వయంగా నివసించకుండా కిరాయకు ఇచ్చినట్టయితే ఇంటి ఋణం పై వడ్డి పూర్తిగా మినహాయింపు కలదు, కాని వచ్చే కిరాయిని ఆదాయంగా చూపాలి.

U/s 24 and 80 EE: There is an Exemption for interest on housing loan (for Self-occupied Residence). If the loan was taken before Apr 1, 1999 exemption is limited to ₹30,000/- per year. If the loan was taken after Apr 1, 1999 exemption is limited to ₹2,00,000/- per year if the house is self-occupied; There is no limit if the house is rented out. This exemption is available on accrual basis, which means if interest has accrued, you can claim exemption, irrespective of whether you’ve paid it or not.. 80EE In finance bill 2016 (an additional rebate of ₹.50.000/- was given to those assesse, who purchase self-occupied single house after 01/04/2016 with maximum value of ₹ 60,00,000 and sanctioned home loan up to 35,00,000)

80 EE: ఎలాంటి ఇల్లు లేకుండా మొదటిసారి ఇంటికొసం పైనాన్సియల్ ఇన్స్టిటూషన్ల (బ్యాంకు) నుండి 35లక్షల లోపు రుణం పొంది ఇంటివిలువ 50లక్షల లోపు ఉంటూ తేది 01.04.2016 నుండి 31.03.2017 మద్యన తీసుకున్న రుణం వడ్డీ పై Section 24కి అదనంగా 50,000 వేల మినహాయింపు కలదు.

ఉన్నత చదువుల కోసం విద్యాఋణం పై వడ్డి (80E) : Self, Spouse, Children ఉన్నత చదువుల కోసం విద్యాఋణం పై 2017-18 ఆర్ధిక సంవత్సరం లో చెల్లించిన వడ్డి మినహాయింపు కలదు. ఈ మినహాయింపు గరిష్టం గా 8సం. లు వర్తిస్తుంది.

ఆదారపడిన వారు వికలాంగులయితే (80DD) : ఆదాయపు పన్ను చెల్లించే వ్యక్తిపై ఆదారపడిన వాళ్ళలో వికలాంగులుంటె సెక్షన్ 80DD క్రింద మినహాయింపు కలదు. 80% కన్నా తక్కువగా వైకల్యం ఉంటె 75,000/- , 80% లేదా అంతకన్నా ఎక్కువ వైకల్యం ఉంటె 1,25,000/- మినహాయింపు కలదు. ఇందుకోసం సంబందిత అధికారులు జారిచేసిన సర్టిఫికేట్ పొంది ఉండాలి.

ఆదాయపు పన్ను చెల్లించె వ్యక్తీ వికలాంగులయితే (80U) : ఉద్యోగి స్వయంగా వికలాంగులైన పక్షంలో 80% కంటే తక్కువ వైకల్యం ఉంటె 75,000/-, 80% లేదా అంతకన్నా ఎక్కువ వైకల్యం ఉంటె 1,25,000/- మినహాయింపు కలదు. వైకల్య ద్రువీకరణ పత్రం సమర్పించాలి.

అనారోగ్యానికి చికిత్సకు అయిన ఖర్చు (80DDB) : ఉద్యోగి కాని తనమీద ఆడరపడిన వారు Cancer, Hemophilia, Talassemia, Neurological diseases మరియు Chronic renal Failure వంటివాటితో అనారోగ్యానికి గురయి చికిత్స కోసం చెల్లించిన సొమ్ములో 60 సంవత్సరాల లోపు వారికి 40,000/-, 60 సంవత్సరాలు లేదా పైబడిన వారికి 60,000/- ,80 లేదా 80సంవత్సరాలు పైబడిన వారికి 80,000/- మినహాయింపు కలదు. దీనికోసం ఫారం 10-I లో సంభందిత స్పెషలిస్ట్ డాక్టర్ చే ఖర్చుల వివరాలు సమర్పించాలి. కాని ఈ సెక్షన్ కింద మినహాయింపు చేసె అవకాశం DDO లకు లేదు.

చందాలు (80G) : PM, CM రిలీఫ్ ఫండ్ వంటి 100% మినహాయింపు గలవాటికి ఇచ్చే చందాలు మినహా , 80G క్రిందకు వచ్చే 50%/30% మినహాయింపులోకి వచ్చే ఏ ఇతర చందాలు DDO లు అనుమతించరాదు.

* Note : సెక్షన్ 80DDB మరియు 80G కింద మినహాయింపు చేసె అవకాశం DDO లకు లేదు. కాని ముందుగా February జీతం తో టాక్స్ చెల్లించి, అధికముగా చేల్లించిన మొత్తాన్ని31 జూలై 2018 లోపు Income Tax Department వారికి SAHAJ ఫారంలో సమర్పించిన తిరిగి చెల్లిస్తారని ఐ.టి. డిపార్ట్మెంట్ వారు గతంలో DTA/DTO లకు సర్క్యులర్ రూపంలో ఆదేశాలు ఇచ్చినారు (vide E.No TDS/clarification/1011 Dt. 15/12/2011 of Addl. Commissioner IT Dept. Hyderabad) తిరిగి పొందవచ్చు.

మెడికల్ ఇన్సూరెన్స్ (80D): ఉద్యోగి తన కుటుంబం కోసం మరియు పేరెంట్స్ కోసం చెల్లించిన మెడికల్ ఇన్సూరెన్స్ వేరు వేరుగా మినహాయింపు పొందవచ్చు. ఉద్యోగి తన కుటుంబం కోసం చెల్లించిన సోమ్ముకాని గరిష్టంగా 25,000/- లు, ఉద్యోగికి మరియు పేరెంట్స్ కి మెడికల్ ఇన్సూరెన్స్ కోసం చెల్లించిన ప్రీమియం కాని గరిష్టంగా 25,000/- , సీనియర్ సిటిజెన్ అయినా ప్రీమియం కాని గరిష్టంగా 50,000/- మినహాయOపు పొందవచ్చు. ఉద్యోగి మరియు పేరెంట్స్ కోసం మాస్టర్ హెల్త్ చెకప్ కోసం సొమ్ము ఉపయోగిస్తే ఈ సెక్షన్ కింద గరిష్టం గా 5,000/- మినహాయింపు కలదు. ఉద్యోగి కుటుంబ సభ్యులకు మరియు పేరెంట్స్ కోసం ఈ సెక్షన్ కింద గరిష్టంగా రూ.1,00,000/- వరకు మినహాయింపు కలదు.

కన్వేయన్స్ అలవెన్స్ కి మినహాయింపు కలదు. వృత్తి పన్నుకు పూర్తిగా మినహాయింపు కలదు.

పొదుపు పథకాల పై మదుపు రూ. 1.5 లక్ష :

వివిధ పొదుపు పతకాలలో సేవింగ్స్ (80C) : GPF, ZPGPF, APGLI, GIS, LIC, PLI, National Saving Certificates, Public Provident Fund, Sukanya Samruddhi Yojana, ELSS, ULIPS మొదలయిన పతకాలలో చేసిన సేవింగ్స్, తన, స్పౌస్ ఉన్నత చదువుకోసం, ఇద్దరు పిల్లల వరకు ప్రీ స్కూల్ నుండి ఉన్నత చదువుల వరకు చెల్లించిన ఫీజు, ఇంటి ఋణం పై చెల్లించిన అసలు (Principle), ఇంటిని ఈ ఆర్ధిక సంవత్సరం లో కొన్నవారికి రిజిస్ట్రేషన్ కోసం చెల్లించిన స్టాంప్ డ్యూటీ రూ. 1.5 లక్ష వరకు మినహాయింపు కలదు.

Annuity సేవింగ్స్ పథకం లో సేవింగ్ (80 CCC) : LIC లేదా ఇతర ఇన్సూరెన్స్ ప్రొవైడర్ ల ద్వారా తీసుకున్న ఆన్యుటి స్కీంల కోసం చేల్లించిన ప్రీమియం.

CPS deduction (80CCD): కొత్త పెన్షన్ పై నియామకం అయిన ఉద్యోగులు ప్రతినెల తమ జీతం నుండి 10% చెల్లిస్తున్న CPS deduction 80CCD(1) ప్రకారం మినహాయింపు కలదు. ప్రభుత్వం ఉద్యోగి ప్రాన్ ఖాతా లో జమ చేస్తున్న 10% CPS మ్యాచింగ్ గ్రాంట్ ని 80CCD(2) ప్రకారం జమయిన మొత్తాన్ని పొదుపు రూ. 1.5 లక్షలకు అదనం గా మినహాయింపు కలదు. FY 2015-16 AY 2016-17 లో కొత్తగా 80CCD(1B) సెక్షన్ చేర్చడం జరిగింది దీనిద్వారా కొత్త పెన్షన్ పథకంలో ఉద్యోగి పెట్టిన సొమ్ముపైన 50,000/- వరకు అదనపు మినహాయింపు అవకాశం కల్పించారు ఈ సదుపాయం ఏప్రిల్ 2016 నుండి అందుబాటులోకి వచ్చింది. ఈ సెక్షన్ పైన పలువురు పలు సందేహాలు వ్యక్తపరచగా మన రాష్ట్ర శాఖ వారు 2 సందర్భాల గురించి ఆదాయపన్ను శాఖ వారి నుండి క్లారిఫికేషన్ కోరగా ఆదాయపన్ను శాఖ వారు F.No. Pr. CCIT/Tech/67/2015-16 తేదీ 12.02.2016 సమాధానం ఇచ్చినారు అవి 1. ఒక ఉద్యోగికి 80సి కింద CPS నిది కాకుండా 1.50 లక్షల పొదుపు నిధి ఉన్నప్పుడు CPS కింద ఉద్యోగి జమచేసిన నిధిని 80CCD(1B) కింద చూపొచ్చా? 2. ఒక ఉద్యోగి 80C కింద పొదుపు CPS (NPS) నిది కాకుండా 1.50లక్షల కంటే తక్కువగా ఉండి CPS (NPS) కింద ఉద్యోగి 50 వేల కంటే ఎక్కువ కొత్త పెన్షన్ కోసం జమచేస్తే ఇట్టి మొత్తాన్ని 80CCD(1B) కింద గరిష్టంగా 50 వేలు పోగా మిగిలిన నిధిని 80C కి విడగొట్టొచ్చా? పై రెండు ప్రశ్నలకు అవును అని సమాధానం ఇచ్చారు.

* 80C, 80CCC, 80CCD ల పొదుపు ల పైన మొత్తముగా 1.5 లక్షలు ఉంటుంది.

సేవింగ్స్ ఖాతా పైన పొందిన వడ్డీ మినహాయింపు (80TTA) : సేవింగ్స్ ఖాతా లో జమయిన వడ్డీ ని ఆదాయం గా చూపిన దాంట్లో నుండి వడ్డీని గరిష్టం గా 10,000/- వరకు 80TTA ప్రకారం రూ. 1.5 లక్ష సేవింగ్స్ పై అదనముగా 10,000/- వరకు మినహాయింపు అవకాశం ఉంది. ఈ ఆర్థిక సంవత్సరం నుండి సెక్షన్ 80TTB ప్రకారం ఆదాయపన్ను చెల్లింపుదారులు సీనియర్ సిటిజెన్ అయితే 50వేలు వరకు మినహాయింపు కల్పించారు.

* Note : DDO లు ఫిబ్రవరి మాసం జీతం బిల్ పొందే సమయములో Form-16 లు సమర్పిస్తు డిడక్ట్ చేసిన ఇన్కమ్ టాక్స్ TAN నెంబర్ తో జమ అవుతుంది, దీనికి సంబందించిన బిన్ నంబర్స్ STO/ Online లో TAN నెంబర్ ద్వారా తీసుకుని ఉద్యోగి వారిగా CA తో ఇ-పిల్లింగ్ ద్వారా TDS వివరాలు వివరాలు 31 జూలై,2019 లోపు ఆన్లైన్ చేయించాలి, ఇలా చేయని వారికి Income Tax Department వారు ఫైన్ వేసే అవకాశం ఉంది. ఆదాయపు పన్నుకు సంబంధించి ఏఏ ఫారములు సమర్పించాలి? జనవరి, ఫిబ్రవరి మాసములలో మీ సేవింగ్స్ మరియు మినహాయింపులను తెలుపుతూ Form-12BB పూర్తిచేసి DDO లకు ఇవ్వాలి. వాటిని పరిగణలోకి తీసుకుని, నెలవారీగా చెల్లించిన జీతం మరియు జీతం ద్వారా చేసుకున్న

పొదుపుల ఆధారంగా DDO లు Form-16ని తన పరిధిలోని ఉద్యోగులకు ఇవ్వాలి. ప్రతి ఉద్యోగి ఆదాయపు పన్ను పరిదిలోకి రాకపోయినా “PAN” కార్డ్ విదిగా పొందాలి. దీనికొరకు దగ్గరలోని CA ని సంప్రదించండి. నికర ఆదాయము రూ. 5లక్షల కంటే ఎక్కువ ఉన్న వారు, బ్యాంకు, పొస్టాఫీసులలో 10,000/- ల కంటే ఎక్కువ ఆదాయము కలిగిన ఉద్యోగులు మరియు ఒక ఎంప్లాయర్ కంటే ఎక్కువ ఎంప్లాయర్స్ వద్ద జీతం పొందు వారు “ITR” ఫారములలో రిటర్న్ లను 31జూలై, 2019 లోపు Income Tax Department వారికి సమర్పించాలి.

ఆదాయపు పన్నుని ఎలా చెల్లించవచ్చు?

Advance Tax: మనం సంబంధిత ఆర్థిక సంవత్సరానికి చెల్లించాల్సిన ఆదాయపు పన్ను 10,000 కంటే ఎక్కువ ఉంటే తప్పనిసరిగా ముందస్తుఆదాయపు పన్ను చెల్లించాలి. ముందస్తు పన్ను త్రైమాసికముల వారిగా చెల్లించాల్సిన శాతాన్ని మరియు చెల్లించాల్సి గడువులను ఆదాయపు పన్ను డిపార్ట్మెంట్ వారు తేదిలను ఇచ్చారు అవి క్రింద చూపడం జరిగింది. ఈ ముందస్తు పన్ను చెల్లింపు నుండి 60సంవత్సారలులేదా అంత కంటే ఎక్కువ వయస్సు కలిగి ఉండి ఎలాంటి బిజినెస్ చెయనివారికి మినహాయింపు కలదు. ఆదాయపు పన్నుని శ్లాబులకనుగుణముగా తాత్కాలికంగా మదింపు చేసి సుమారుగా చెల్లించవలసిన ఆదాయపు పన్ను తెలుస్తుంది. ఈ మొత్తమును ప్రతి నెలలో కొంత చొప్పున DDOలు ప్రణాళిక బద్దంగా ఆన్లైన్ జీతాల బిల్లులో మినహాయించి క్వార్టర్ వారీగా e-TDS చేయించాలి. ప్రతినెల DDO నుండి ఐ.టి. మినహాయించి షెడ్యుల్ ను (టోకెన్ నం. తేది తో సహా) తీసుకుని భద్రపరచుకోవాలి. పిబ్రవరి నెలలో 4 వ క్వార్టర్ కి సంబందించిన చెల్లించాల్సిన ఆదాయపు పన్ను Form-16 ప్రకారము మదింపు చేసి అధికముగా చెల్లించవలసినది ఏమైనా ఉంటె పిబ్రవరి 2020 నెలలో మినహాయించుకోవచ్చు. షెడ్యుల్ లో PAN తప్పనిసరిగా పొందుపరచాలి.

(adsbygoogle = window.adsbygoogle || []).push({});

APPSC Group I, Group II, Group III, Group IV Final Syllabus, Exam pattern psc.ap.gov.in

APPSC Group 2 Mains Hall Tickets- Exam Dates Admit Card 2019 download @psc.ap.gov.in